What Is a Fair Credit Score and How Can It Help You?

Is a fair credit score good?

If your credit score falls into the “fair” range, lenders could view you as a subprime borrower or a financial risk and may hesitate to offer you a line of credit. Lower scores indicate a less-than-desirable credit history, and lenders could consider those with fair scores more likely to default on loans.

You might still qualify for credit cards and loans with a fair score, but they will likely come with higher-than-average interest rates and up-front deposits. In fact, borrowers with fair scores pay about much more in interest on credit cards and other loan types than borrowers with very good scores. Some lenders might even reject your application altogether if your score falls below their minimum requirement for approval.

To avoid this, you should try to improve your credit. Moving your score into a higher category over time could earn you lower interest rates on home, student and personal loans and increase your chances of approval when submitting rental applications.

Fortunately, for those with a lower score, lenders also consider other factors when calculating the risk associated with lending to the individual, such as proof of income or employment history. Minimum requirements for approval also vary by lender, so a lower credit score doesn’t automatically disqualify an individual from taking out credit.

What is the average credit score?

The average FICO score in the U.S. was 714 as of Q3 2022. An average FICO score of 711 falls into the “good” category, indicating that an increasing number of Americans have a credit score that is either good, very good or exceptional.

That said, lenders don’t consider the national average when deciding what an acceptable credit score is. It can be helpful to see how your score stacks up, but the national average won’t affect your chances of being approved for new credit.

What lowers your credit score?

If your credit score is lower than you want it to be, it’s important to consider what factors might be hurting it. Some of the most common actions that cause credit scores to drop include missing payments, defaulting on accounts and consistently using more than 30 percent of your available credit.

Applying for a lot of credit in a short period can also hurt your score. Credit inquiries remain on your report for two years, and many inquiries showing up at once could indicate to lenders that you are in a tough financial situation or have applied for more credit than you can handle. Once you have identified the actions hurting your credit, you can start taking steps to remedy them.

Fair vs. good credit score

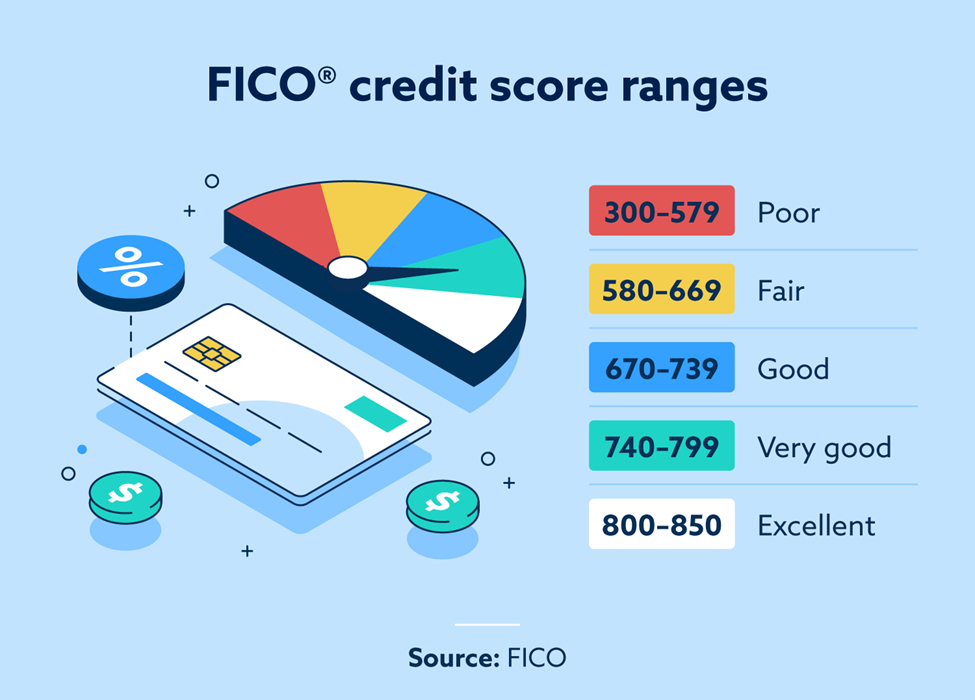

When it comes to applying for loans and opening new lines of credit, a good credit score can qualify you for fantastic opportunities. Good credit is one rung above fair credit and one level below very good credit, according to FICO. However, individuals with fair credit shouldn’t feel discouraged—having a score within the 580 to 669 range can still qualify you for better loans than you may have been restricted to if you had poor credit.

And fortunately, it’s possible to gradually transform a fair credit score into a good one by practicing responsible financial habits.

How to improve your fair credit score

Fortunately, credit scores can easily change over time. You can access your credit report for free each year from Equifax®, Experian® and TransUnion® to identify improvement areas. Once you note any factors that could be hurting your credit, try the following steps to improve your chances of qualifying for better terms and rates over time.

Keep your credit utilization ratio low

Your credit utilization ratio refers to the percentage of available credit that you are using at any given time. Try to keep your credit utilization percentage below 30 percent. It could improve your credit, and lenders will be more likely to approve your future credit applications.

Pay bills on time

Your payment history makes up 35 percent of your FICO credit score, so it’s important to pay your bills on time if you want to improve your credit. If you’ve struggled to pay on time, consider setting up automatic payments. It’s also important to get current on any late payments as soon as you can.

Check your credit reports and dispute any errors

Inaccuracies appear on credit reports more often than you might think. Inaccurate information could harm your credit, so it’s important to regularly monitor your reports from all three credit bureaus and dispute any errors. The process is free and should not hurt your credit.

Consult a credit repair consultant

If you’re struggling to improve your credit on your own, consider seeking out a credit repair consultant. They can help you design a plan to manage your credit and improve your credit over time. Seeking out credit repair services will also not hurt your credit. Knowing how a fair credit score can impact your chances of approval is the first step in the process of better managing your credit. If you want to start improving your credit, remember to regularly monitor your credit reports, stay up to date on your payments and address errors or seek out a credit repair service when you notice inaccuracies on your credit reports.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.