VantageScore vs. FICO Score: How Are They Different?

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

VantageScore® and FICO® use somewhat different factors to determine credit scores. They also have separate requirements for credit history and distinct credit score ranges.

VantageScore® and FICO® are both accurate credit scoring models with unique nuances. For example, FICO treats credit mix and age of credit as two separate categories, while VantageScore lumps them into one category (mix and age of credit).

Lenders can use your FICO score and VantageScore when deciding to approve or decline your loan applications. Learning how both models work can help you have a positive impact on your credit. We’ll compare and contrast FICO and VantageScore to help answer questions like “Why are my credit scores different?”

Key takeaways

- VantageScore and FICO are both accurate scoring models that use different factors to calculate your credit score.

- FICO was established in 1981, while VantageScore was founded in 2006.

- Payment history impacts VantageScores and FICO scores the most

Table of contents:

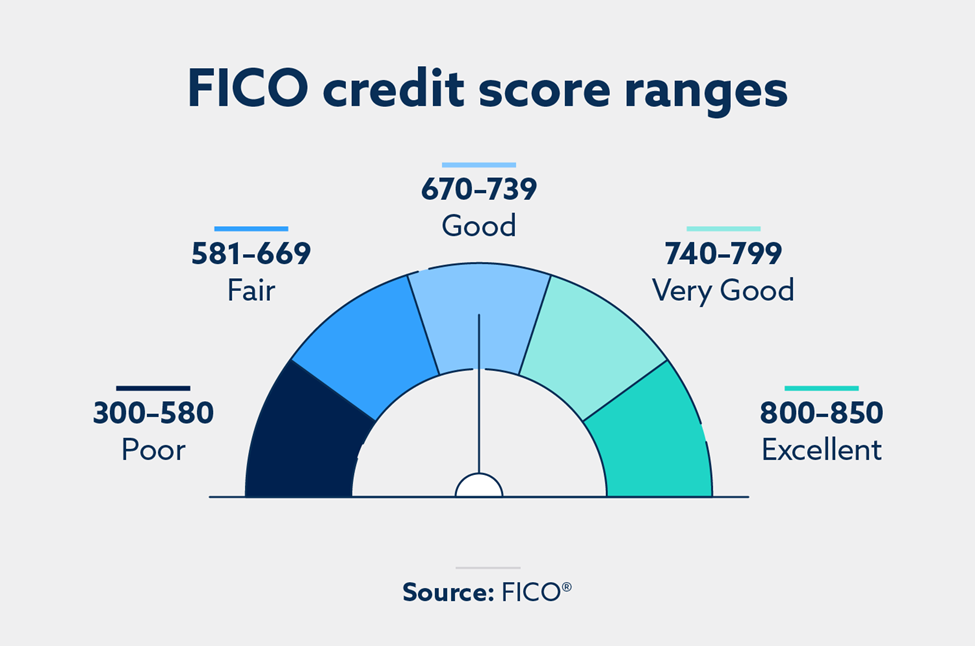

What is a FICO score?

Your FICO credit score is a credit scoring model created by the Fair Isaac Corporation (FICO) that is based on information in your credit reports with the three major credit bureaus—Equifax®, Experian® and TransUnion®. FICO score 8 is the most popular version of this model, and other versions can specifically weigh your habits with auto loans and credit cards.

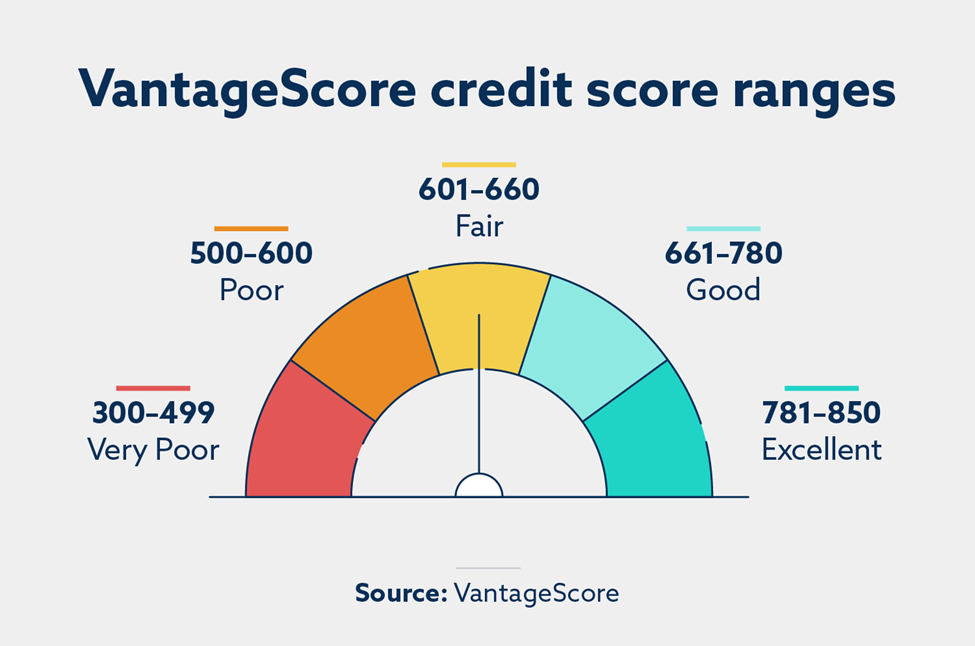

What is a VantageScore?

Your VantageScore is also based on information in your credit reports with the three major credit bureaus, and it was created by those same credit bureaus as an alternative to the FICO scoring model. VantageScore 3.0 is the most commonly used version of this tool, which debuted in 2013. VantageScore 4.0 incorporates machine learning to analyze a person’s credit habits over time.

Why are my FICO score and VantageScore different?

There are multiple reasons why your FICO score and VantageScore may differ, and it comes down to the way each model calculates scores. Here are several ways that these popular scoring models differ from each other.

Creation and history

The Fair Isaac Corporation was founded in 1956 (then called Fair, Isaac and Company), and they created the FICO score model in 1981. The corporation’s long-standing history is one of the reasons why so many lenders use its scoring models.

VantageScore Solutions, LLC, created the VantageScore model to gauge your creditworthiness using a different formula than FICO. This model was created in 2006, and many lenders have adopted it since.

Minimum scoring criteria

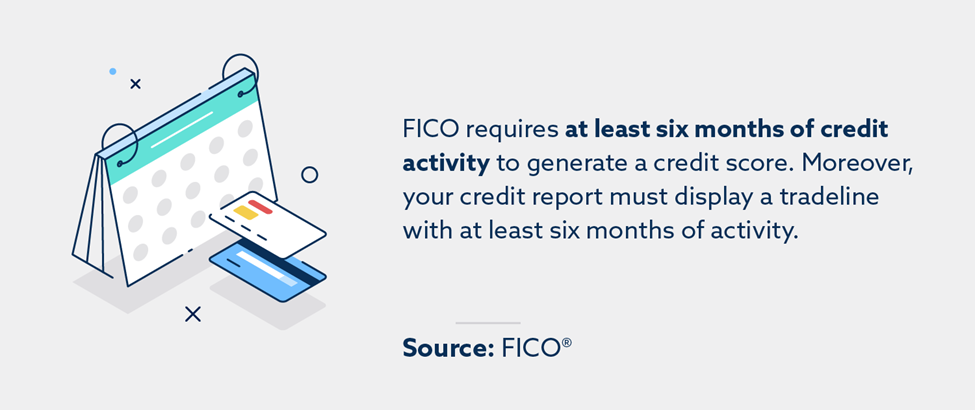

FICO requires at least six months of credit activity to generate a credit score. Moreover, your credit report must display a tradeline (which refers to an item such as a credit card or line of credit) with at least six months of activity.

VantageScore simply asks that clients have at least one tradeline item on their credit reports. There’s also no minimum monthly requirement for that item.

Credit score values

When comparing your VantageScore vs. FICO score, knowing which factors affect each model is important.

FICO Score 8 consists of the following five factors:

- Payment history (35 percent): Gauges how often you make payments on time.

- Accounts owed (30 percent): Weighs how much of your available balance you’ve used.

- Credit age (15 percent): Measures the average age of your open credit accounts.

- Credit mix (10 percent): Indicates how diverse your open credit accounts are.

- New credit (10 percent): Looks at any new credit accounts you’ve applied for.

VantageScore 3.0, on the other hand, looks at these six metrics:

- Payment history (40 percent): Weighs your on-time payments and your missed payments.

- Depth and age of credit (21 percent): Measures your credit mix and the average age of your credit.

- Credit utilization (20 percent): Is the same as FICO’s “accounts owed” category.

- Total balances (11 percent): Looks at your outstanding balances across all accounts.

- Recent credit (5 percent): Examines your behavior with new credit.

- Available credit (3 percent): Refers to how much credit you currently have available.

Based on these factors, it’s easy to see why your FICO score and VantageScore can differ. Credit mix is scrutinized by VantageScore far more than FICO, which is why it can help to responsibly manage different credit accounts. FICO, on the other hand, weighs new credit activity more heavily—so pace yourself when applying for new credit.

Is your FICO score or VantageScore more important?

Your FICO score and VantageScore are both important because they can help you get a sense of your current credit habits. However, auto loan lenders, commercial banks and landlords favor FICO. This means that your application for a new rental property will likely be approved or declined based on the strength of your FICO credit score.

There’s a lot of overlap between FICO and VantageScore, so most credit-building tips apply to both models. For example, payment history is the most important factor for both FICO and VantageScore, so making timely payments will positively impact both scores.

Several other ways to increase your credit scores include:

- Frequently check your credit report to dispute errors and review your habits.

- Limit the number of credit cards or loans you apply for all at once.

- Learn how Lexington Law Firm’s focus tracks can help you rebuild your credit after major life events.

Monitor your credit with Lexington Law Firm

Responsible credit habits will build your credit no matter which model is being taken into account. Lexington Law Firm can help you better understand your current credit habits, help you manage account inquiries and address errors on your credit reports.

Learn more about our services and see if they will suit your needs.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.