How to Build Credit as a Student

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

Learning how to build credit as a student is important so you’re ready for life after graduation. Focus on building healthy credit habits—paying bills on time, keeping your credit utilization low and avoiding common credit mistakes.

While the government considers you an adult at 18, many people consider graduating college and starting their first job as the first real marker of adulthood. However, adulthood comes with responsibilities, many of which require a credit score—putting utilities in your name, renting your first apartment, putting car insurance in your name and even buying a car.

Read on to learn about some of the ways you can build credit as a student so you can graduate college with a degree and healthy credit.

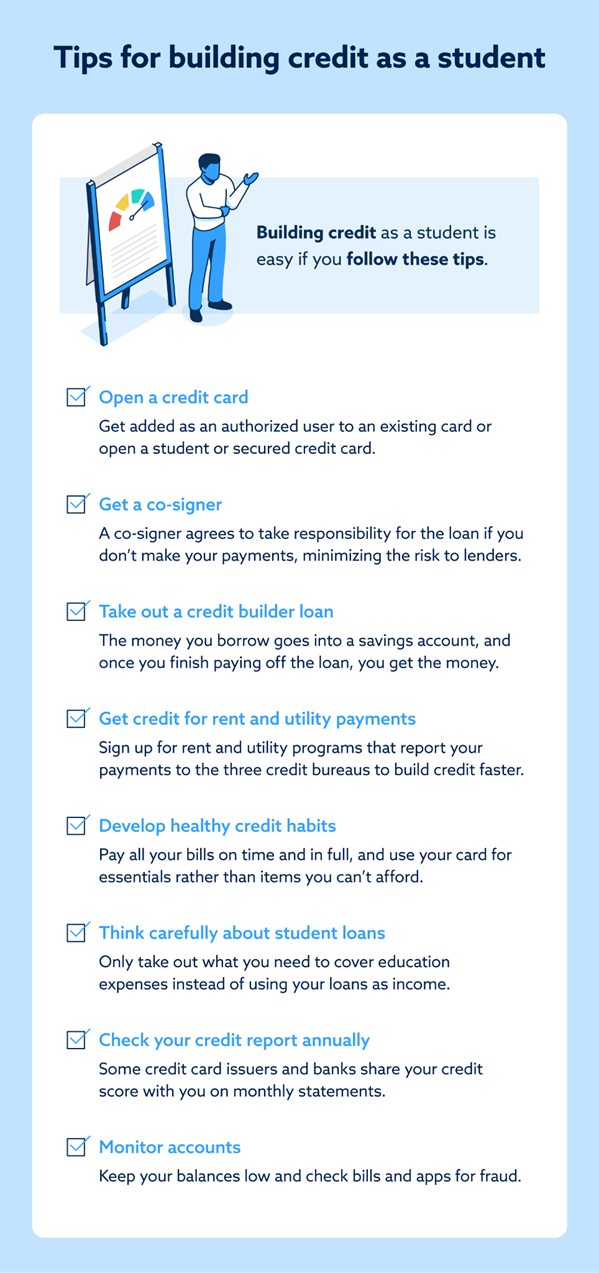

Become an authorized user on a credit card

For many students, the first step to building credit is using a credit card to build credit. Unfortunately, it can be challenging to get a credit card if you don’t have any credit.

Often, a person’s first credit card isn’t actually theirs. Instead, they become an authorized user on someone else’s credit card. An authorized user is someone who is added to another person’s credit card account with full spending privileges. Responsibility for paying the credit card bill will still belong to the primary cardholder, who is usually a parent, close friend or relative.

The advantages to being an authorized user don’t end with being able to use the card like it’s your own. You also piggyback credit because the credit card’s account and payment histories are added to your credit report. This extends the length of your credit history, builds your payment history and increases the amount of credit available to you, which should all help improve your credit.

If you want to ask someone to make you an authorized user on their account, make sure they have a good credit history. You don’t want to be added as an authorized user to a primary cardholder who doesn’t pay their bills on time, since that would hurt your credit more than help it.

Open a student credit card

If you can’t become an authorized user on someone’s credit card, you can open a student credit card instead. A student credit card is a type of credit card specifically geared for students looking to build credit.

Often, the only difference between a traditional credit card and a student credit card is that they have a lower credit limit. Some also offer rewards for students, such as incentives for good grades and other cashback and rewards offers.

Open a secured credit card

Another type of credit card to consider as a student is a secured credit card. With this type of credit card, you make a deposit to cover your credit limit, which minimizes the risk to the issuer. As a result, credit card issuers are more likely to offer credit to someone with no or low credit.

As you use the credit card and pay your bill on time, you’ll build credit and eventually graduate to an unsecured credit card.

Develop healthy credit habits

College is full of great experiences, but the costs can add up quickly, and being financially responsible can be challenging. Throw in access to credit for the first time, and it’s easy to see why many students struggle with credit initially.

While students may want to take advantage of that new credit limit, it’s important to use your credit card wisely. Only use it for emergencies or small, regular expenses that you have the cash to pay for. These actions seem small, but they will establish the skills you need to keep your credit high throughout your life.

From the moment you have your new credit card, do the following:

- Keep your balance low. This keeps your credit utilization rate low, which is one of the factors impacting your credit health. Experts recommend only using 30 percent or less of your credit limit. An easy way to stick to this is to use your credit card for small, regular purchases each month. For example, put all your subscription services on your credit card or only use it for gas. This habit will also prevent you from overspending or spending money you don’t have on nonnecessities.

- Pay your balance each month. While you are only required to pay off the minimum balance each month, you’ll owe interest on the unpaid balance. The interest is applied to your balance, which can hurt your credit utilization rate, not to mention cost you more over time. Get in the habit now of paying off your entire balance every month.

- Avoid opening too many accounts. Don’t open too many credit cards at once. New credit can damage your credit score, and having too many credit cards can make it harder to monitor your spending.

Take out a credit builder loan

Your credit mix, or the types of credit you have, play a role in your credit score. So, just having a credit card may not be enough to build credit quickly—you need other types of debt. Instead of taking out a loan for a car you don’t need, consider a credit builder loan.

The sole purpose of a credit builder loan is to build credit, so you won’t get money to put toward something else. Instead, the bank will put the money you’re borrowing into a savings account. You’ll make regular payments to repay the loan, and once you’ve satisfied the loan terms, the money in the savings account is yours.

Get a cosigner

When you’re starting to build credit, it may be difficult to get lenders to let you borrow money on your own. You can add a cosigner, someone with a better credit history than you who agrees to take responsibility for the loan if you miss payments. The cosigner minimizes the risk to the lender, making them more likely to lend to you.

As long as you make your monthly payments on time, you can build your credit history and payment history with a cosigner.

Get credit for rent and utility payments

Usually, only credit cards and installment loans such as a student loan or car loan affect your credit. Monthly bills like rent, utilities, and cell phones won’t appear on your credit report unless they’re delinquent.

A few programs and services enable you to add some of your monthly bills to your credit report to track on-time payments and build your credit. For example, ExtraCredit® is a program that reports utility and cell phone bills to credit bureaus, and rent reporting services will add your rent payment history to your credit report.

Only add these bills to your credit report if you pay them on time. Adding them to your credit report and then missing payments will hurt your credit more than help it. Be aware that some of these programs and services may charge a fee.

Think carefully about your student loans

Student loans seem to be a fact of modern life, with over 43.5 million Americans carrying $1.7 trillion in student loan debt. While the exact amount varies, the average student graduate has more than $37,000 in student loan debt.

Using your loan as income might be necessary, but if you can help it, only take out enough to cover your education expenses. Look into work-study or student aid options as alternatives to an oversized loan.

Monitor your accounts carefully

Keep an eye on your accounts to protect yourself from identity theft. By monitoring your account using the credit card app, you can shut down the card as soon as you see fraudulent activity, preventing the problem from escalating.

If you are the victim of identity fraud, you can remove fraud from your credit account.

Check your credit report annually

Experts recommend that you check your credit report and score annually or more often to ensure they’re accurate. AnnualCreditReport.com will give you one free credit report from each of the three credit bureaus at least once every 12 months (currently, you can see your credit reports once a week!).

You can sign up for credit monitoring services if you want to review your credit report more often than once a year. Keep in mind that building credit takes time, and even though you may be able to check your credit score every 14 days with some services, it will still take time to see results.

Avoid these common credit mistakes

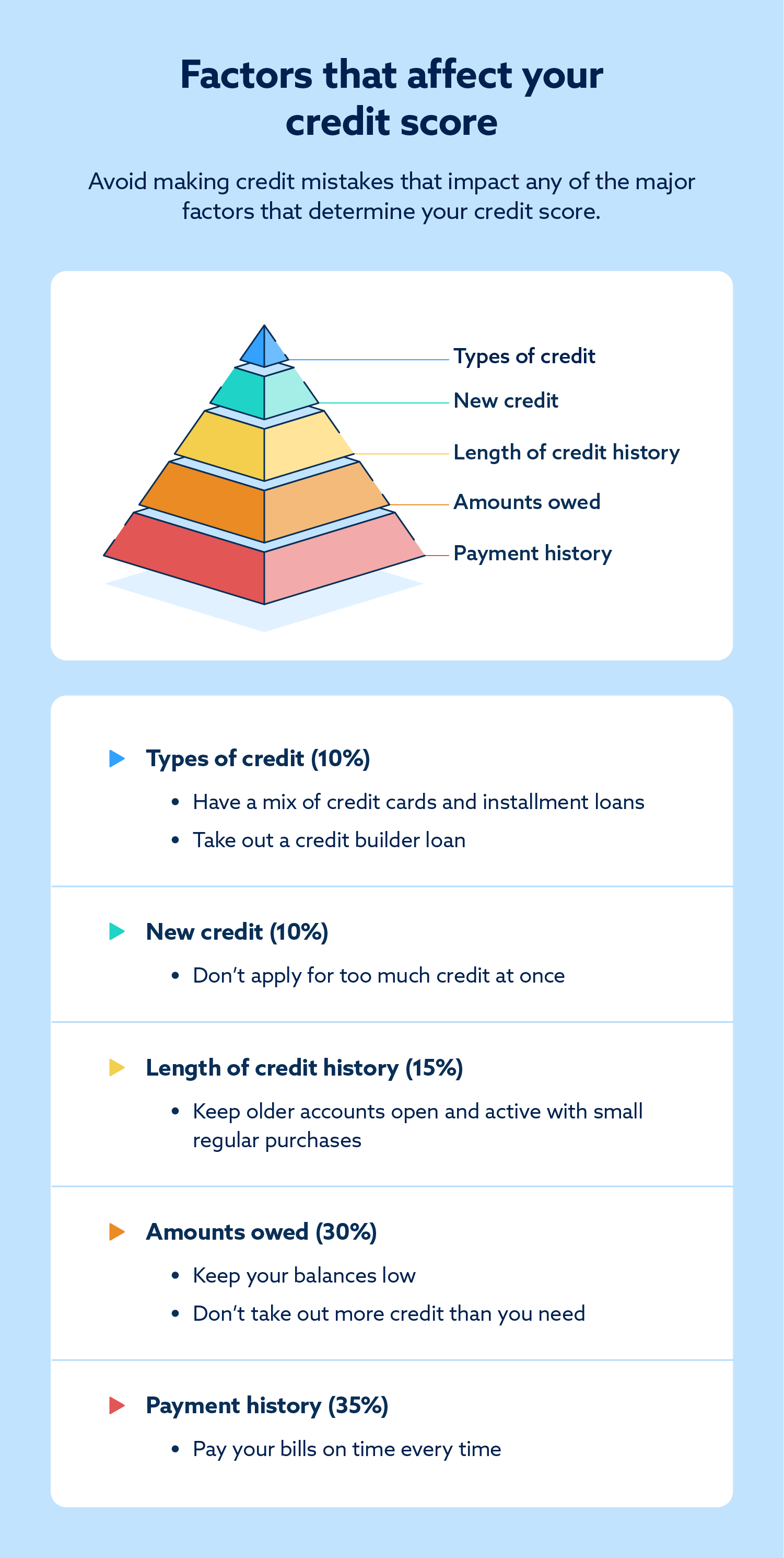

Being a student means learning, and so does building credit. You’ll want to keep the five factors that impact your credit in mind when making decisions. Those five factors are:

- Payment history: 35 percent

- Amounts owed: 30 percent

- Length of credit history: 15 percent

- Credit mix: 10 percent

- New credit: 10 percent

While mistakes are part of the learning process, you’ll want to avoid these common credit mistakes to avoid long-term consequences to your credit.

Mistake #1: Waiting too long to start building credit

Credit factor: Payment history

Most experts agree that the best time to start building credit is at age 18. The length of your credit history determines 15 percent of your FICO credit score. If you start building credit at 18, you’ll have around four years of credit history by the time you graduate and need to start putting bills and loans in your name.

Mistake #2: Using your credit card for nonessentials

Credit factor: Amounts owed

When you don’t see the physical money you’re spending, it can be easy to lose track of your spending and spend more money than you have. Avoid this by limiting credit card purchases to essential items only. Use it to pay for groceries and gas, not expensive vacations.

Mistake #3: Maxing out your credit cards

Credit factor: Amounts owed

Maxing out your credit cards hurts your credit utilization rate. The less money you carry from month to month, the better it is for your credit.

If you have a low credit limit, you can avoid maxing out your card by paying more often than the monthly payment due date. For example, if you buy gas and groceries over the weekend, check your balance on your credit card app a few days later and pay it off.

Mistake #4: Missing payments

Credit factor: Payment history

If you aren’t used to them, remembering to pay monthly payments at first might be rough. But you want to avoid late payments at all costs because they can hurt your credit for up to seven years.

Avoid missing payments by setting up automatic payments or calendar reminders on your phone. If you missed the payment because it didn’t line up with your paycheck and you didn’t have the money, you may be able to change your payment date with the credit card company.

Mistake #5: Closing accounts too soon

Credit factor: Length of credit history

If you open a student or secured credit card and graduate with a traditional credit card, it might be tempting to close those other accounts. But if you don’t have any additional credit beyond those initial credit cards, closing them can actually hurt your credit health by minimizing the length of your credit history.

Instead of closing them and opening new credit cards, see if your credit card issuer can convert the student or secured credit card account to a traditional one. That way, you can keep the account active and preserve the length of your credit history.

If you can’t convert the account, hold onto it and make a small purchase every month to keep it active. After you’ve had the new credit card for a while, you can cancel your initial credit cards.

Mistake #6: Taking out too much credit

Credit factor: Amounts owed

Just because someone offers you credit doesn’t mean you should take it. Sometimes lenders offer more money than you need because they make money off your interest payments. When considering credit offers, look carefully at monthly payments and consider your budget. Only take out credit for the amount you need and can reasonably afford to pay back each month.

For example, when you apply for an auto loan for your first car after college, the lender might preapprove you for $20,000. Run the numbers and ensure that’s a monthly payment you can afford. You’ll probably find that you can only comfortably afford to borrow a lower amount.

FAQ

Here are some answers to common questions about how you can build credit as a student.

How long does it take for a student to build credit?

Typically, it takes about six months to a year to build up some credit. Your exact timeline may vary based on your specific situation and how responsible you are with credit-building techniques like a student credit card.

How can a college student build credit with no income?

Usually, you’ll need income to qualify for credit, but there are a few ways around it. You can use a cosigner for a loan or ask someone to add you as an authorized user to their credit card. As an authorized user, you won’t have to make any payments with your credit card to get the card put on your credit report.

Trust Lexington Law Firm to fight for your credit

Building credit is tough—it’s hard to build from scratch but frustratingly easy to damage. Don’t let a lack of credit or a few credit mistakes destroy your confidence. The credit repair team at Lexington Law Firm could help you challenge inaccuracies affecting your credit. Learn more about our services to see how we can help.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.