How Can You Pay a Loan with a Credit Card?

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations.

Can you pay a loan with a credit card? Yes, paying a loan with a credit card is sometimes possible. Yet, whether or not you can do so depends on factors such as the lender’s policies or the type of loan you want to pay off.

Are you looking for a creative way to pay off your loans? If you hope to get extra travel points while reducing your monthly payments, you might wonder, “Can you pay a loan with a credit card?”

This post will delve into the types of loans you can pay off with a credit card and the pros and cons of making these payments.

In This Piece:

Can I Pay a Loan with My Credit Card?

Whether or not you can pay a loan with a credit card depends on various factors, including the lender’s policies and the type of loan you wish to pay off.

While some lenders may allow credit card payments, others may not accept them. Understanding the terms and conditions of your loan agreement before attempting to pay it off with a credit card is crucial.

Which Loans and Debts Can I Pay with a Credit Card?

You can use credit cards to pay off different loan types, providing flexibility and potential benefits. Here are some common types of loans you can typically pay with a credit card:

- Personal loans: These unsecured loans can often be paid with a credit card, allowing you to consolidate debt or manage your monthly payments conveniently.

- Medical Bills: Many healthcare providers accept credit card payments for medical expenses, allowing you to pay off medical bills over time.

- Small Business Loans: If you have a small business loan, check with your lender to see if credit card payments are accepted. This option can offer cash flow management advantages for entrepreneurs.

- Balance Transfers: While not a specific loan, balance transfers are a preferred method. They allow you to move existing credit card debt to a new card with a lower interest rate, potentially saving you money in the long run.

Pros and Cons of Paying Loans with Credit Card

Using a credit card to pay off loans has its own advantages and disadvantages. Let’s explore both sides to help you make an informed decision.

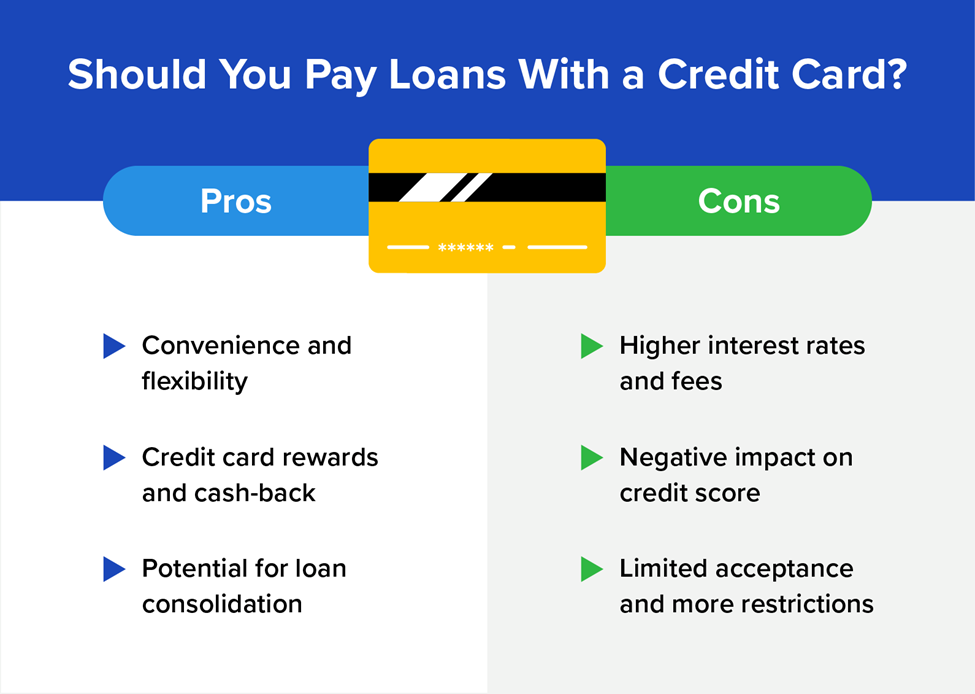

Pros

- Convenience and flexibility: Paying a loan with a credit card provides convenience and flexibility, allowing you to manage your debt from a single source. It simplifies your monthly payments and can help you stay organized.

- Rewards and cash back opportunities: Some credit cards offer rewards programs or incentives, allowing you to earn points or money back on your loan payments. This can be beneficial if you use your credit card responsibly and take advantage of these perks.

- Potential for consolidation: If you have multiple loans or high-interest debts, paying them off with a credit card can consolidate your debt into a single monthly payment. This simplifies your financial obligations and may allow you to save on interest charges.

Cons

- Higher interest rates and fees: Credit cards typically have higher interest rates than other loan types. If you cannot completely pay off the credit card balance each month, you may incur significant interest charges, which can offset any rewards or benefits.

- Impact on credit score: Utilizing a large portion of your available credit can impact your credit score negatively. Additionally, applying for new credit cards to pay off loans may result in hard inquiries on your credit report, potentially lowering your score.

- Limited acceptance and more restrictions: Not all lenders accept credit card payments, and some may impose restrictions or fees for using this method. It’s essential to confirm with your lender before attempting to pay off a loan with a credit card.

Then, is it a good idea to pay a loan with a credit card? It depends on your unique circumstances. It can be advantageous in certain situations, such as consolidating high-interest debts or taking advantage of rewards programs.

However, it’s crucial to consider the interest rates, fees, and potential impact on your credit score. Assessing your financial goals and consulting with an advisor can help determine if this approach aligns with your financial well-being.

How to Pay a Loan with a Credit Card

If you’ve decided to pay off a loan with a credit card, follow these steps:

- Review loan terms: Confirm that your lender accepts credit card payments and inquire about any associated fees or restrictions.

- Assess your credit card’s terms: Check the interest rate, credit limit, and any balance transfer options on your credit card. Ensure that the card’s terms align with your financial goals.

- Calculate feasibility: Determine if paying off the loan with a credit card is financially feasible based on the interest rates, fees, and your ability to repay the credit card balance promptly.

- Contact your lender: Inform your lender of your intention to pay the loan with a credit card and follow their instructions for making the payment.

- Make payments promptly: Pay your credit card bill on time to avoid additional interest charges and late fees.

FAQs

Many questions come up regarding paying loans with a credit card, but there are four common questions people always seek answers for. Let us take a look.

Can You Pay a Mortgage with a Credit Card?

In most cases, paying your mortgage with a credit card is impossible. Mortgage lenders typically require payments through bank transfers, checks, or online bill payment methods. However, you may be able to indirectly use a credit card by utilizing balance transfer checks or money transfer services to pay off a mortgage. Before considering this option, assessing the fees, interest rates, and credit card terms is essential.

Can You Pay Off a Car Loan with a Credit Card?

Car loan lenders generally do not accept credit card payments directly. Like mortgage payments, you can typically make car loan payments through bank transfers or other approved payment methods. However, you may be able to use a credit card to indirectly pay off a car loan by employing balance transfer checks or money transfer services. Evaluate the feasibility and costs associated with this approach before proceeding.

Can You Pay a Student Loan with a Credit Card?

Paying student loans with a credit card is usually not possible. Most student loan servicers do not accept credit card payments because they have high transaction fees. However, you can explore alternative options such as balance transfers or personal loans to pay off student loans. It’s crucial to evaluate the interest rates, fees, and terms of these options before proceeding.

Can I Use a Credit Card to Pay Off Payday Loans?

While it’s possible to use a credit card to pay off a payday loan, it’s generally not advisable. Payday loans can come with high interest rates, and adding credit card interest can lead to significant debt.

Exploring other alternatives for paying off payday loans is recommended, such as negotiating a repayment plan with the lender or seeking assistance from credit counseling organizations.

In conclusion, paying off a loan with a credit card can be a viable option depending on your specific circumstances. It offers convenience, flexibility, and potential rewards or debt consolidation benefits. However, it’s essential to consider the higher interest rates, fees, and potential impact on your credit score.

Assess your financial situation by consulting with professionals if needed, and ensure that your credit card terms align with your goals. To find the right credit card and loans, visit our credit cards and personal loans. Empower yourself to take control of your credit and achieve your financial well-being.