How to Build Credit With a Secured Card: 6 Tips for Success

The information provided on this website does not, and is not intended to, act as legal, financial or credit advice. See Lexington Law’s editorial disclosure for more information.

To build credit with a secured credit card:

1. Keep your balance low.

2. Use it only for small regular purchases.

3. Monitor your spending.

4. Pay off the entire balance each month.

Whether you’re a teenager trying to start building credit or looking to rebuild your credit after some bad luck, it can be difficult to get creditors to give you opportunities. You know you need to build credit, but you can’t do it if no one will issue you credit. Fortunately, you can use a tool like a secured credit card.

Wondering how to build credit with a secured credit card? Read on to learn everything you need to know to start turning your credit around.

Table of contents:

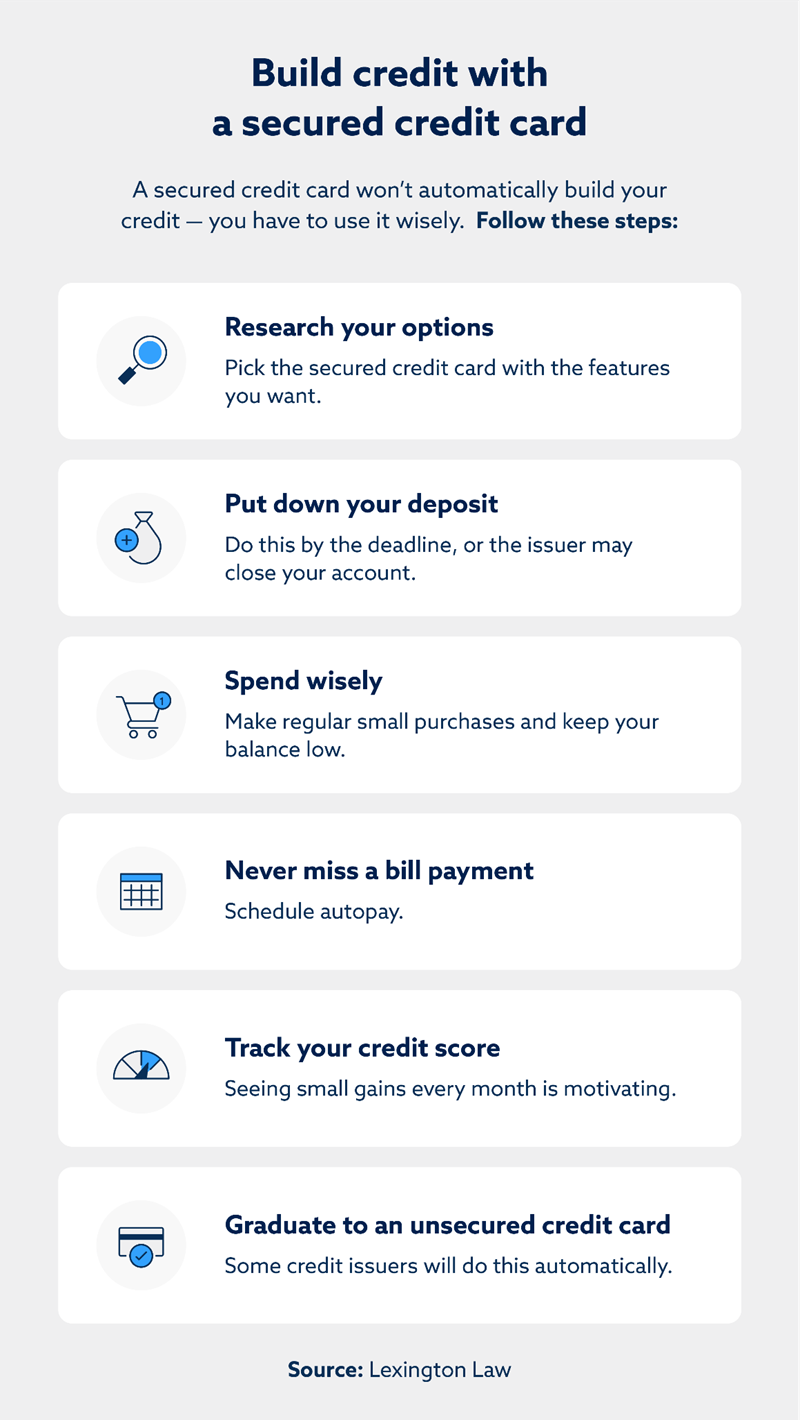

- Research your options

- Put down your deposit

- Spend wisely on your secured credit card

- Never miss a bill payment

- Track your progress on your credit report

- Use your improved credit to graduate to an unsecured credit card

What is a secured credit card?

A secured credit card is just like a regular credit card, but it requires a deposit that covers the spending limit. Since the deposit will cover what you owe if you don’t pay your credit card bill, it reduces the credit card issuer’s risk when extending you credit.

It’s just like when your landlord requires you to pay a security deposit to cover any damages to the apartment. Even if you leave without paying for the repairs, the landlord can cover them using your security deposit.

Use the tips below to help you use your secured credit card responsibly and build your credit.

1. Research your options

Don’t sign up for just any secured credit card. Take the time to find the best secured credit card for your situation and carefully consider the pros and cons of secured credit cards before applying.

Start the process by checking your credit. While secured credit card issuers are more likely to extend you credit no matter your credit score, not all do. Make sure you know what your credit score is before applying.

Armed with your credit score, take some time to research different secured cards. While most secured credit cards don’t offer the same features as unsecured credit cards, you’ll find a few that do.

Consider which of the following features are most important to you:

- Flexible deposits

- Low annual fees

- Automatic account reviews to determine if you’re ready for an unsecured credit card

- No credit check (note that this may come with a higher annual fee)

- Reward or cash back options

Finally, consider any potential costs associated with unsecured credit cards. Discover if the deposit is refundable and if there are any application or annual fees.

Once you’ve decided on a card, fill out the application and send in the application fee (if there is one).

2. Put down your deposit

After you’ve been approved, the credit card issuer will tell you your credit limit and ask you to pay your deposit. Make sure you do so quickly—if you don’t get your deposit in on time, they may close your account before you have a chance to use it.

Remember, the amount you’ll have to deposit will depend on your credit card issuer. Some secured credit card issuers require your deposit to cover the entire credit limit, while others may only require you to put down half of it. Some companies also allow you to raise your credit limit by increasing your deposit, while others aren’t as flexible.

3. Spend wisely on your secured credit card

After making your deposit, you can use your secured credit card like you would any other credit card to build credit. You can use your secured card to make purchases anywhere that takes a credit card, and when you hand your card to the sales clerk to make your purchase, they won’t be able to tell it’s a secured card.

But if you want to improve your credit, you must use your secured card wisely. Keep the following tips in mind:

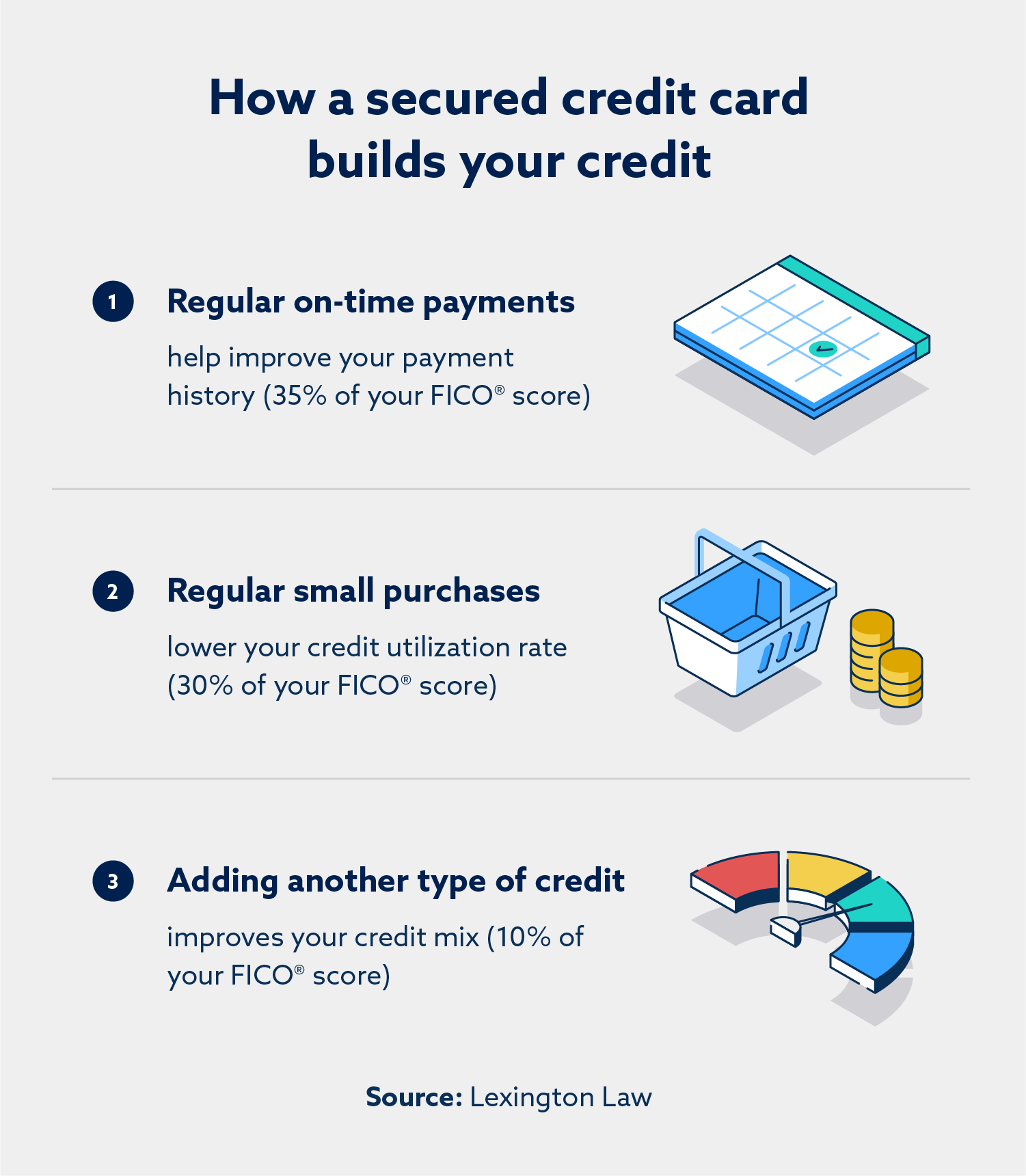

- Make regular small purchases with your secured card. Consider using your card for one type of purchase, such as gas or monthly subscriptions. This will keep your balance low while also keeping your spending in check.

- Keep the balance as low as possible. Experts typically recommend keeping it below 30 percent, but since you’re actively working to improve your credit, try only using 10 percent of your available credit. This means that if your card has a limit of $1,000, you should keep your balance below $100. Small regular purchases will help you accomplish this.

4. Never miss a bill payment

The deposit on your secured credit card does not cover your purchases, so you still need to pay your monthly bill. While you are only required to pay the minimum balance, make it a habit to pay the entire balance off each month.

This will keep your credit utilization low and help you avoid paying interest on an unpaid balance. Avoiding interest charges is especially important on secured credit cards since they often carry higher interest rates than unsecured credit cards.

5. Track your progress on your credit report

As you use your secured credit card, monitor your credit score closely. While increasing your credit may be a slow process, seeing small gains can be motivating. Plus, it will help you ensure your credit report is accurate.

Some credit card companies are starting to offer credit monitoring services and include your credit score on your bill. If your credit card issuer doesn’t offer this, you can see your credit report at AnnualCreditReport.com.

6. Use your improved credit to graduate to an unsecured credit card

As your credit improves, you can upgrade to an unsecured credit card. Some companies also refer to this as “unsecuring” or” graduating” to an unsecured credit card.

Some secured credit card issuers will automatically upgrade you to an unsecured credit card, at which point they’ll usually apply your security deposit as a statement credit offsetting your purchases. You can also apply for an unsecured credit card, at which point you’ll close the secured credit card and the issuer will refund your deposit. The best time to upgrade to an unsecured credit card is when you feel confident in your credit card habits. You want to ensure you can use the credit card responsibly to keep building your credit.

What are the benefits of a secured credit card?

Secured credit cards offer several advantages:

- Most of them report to the three major credit bureaus (Experian®, TransUnion® and Equifax®) so you can build your credit.

- Since the security deposit covers their risk, secured credit card issuers are more likely to issue credit to people with no or poor credit.

- You can gain credit card experience and develop healthy credit card habits.

- Over time, you can work toward an unsecured credit card, which may offer better features.

How long does it take to build credit with a secured credit card?

How long it takes to build credit with a secured credit card depends on several factors, including your credit history and your behavior with the secured credit card. Someone who makes a lot of large purchases on their secured card might see their score improve slower than someone who only makes small purchases, even if both people pay their bills off in full each month.

Typically, it takes six months to a year to see your credit health improve, making a secured credit card one of the best ways to build credit relatively fast. Remember: a secured credit card doesn’t automatically improve your credit—you have to use the card responsibly.

FAQ

Learn more about using secured credit cards to improve your credit below.

How much will a secured credit card raise my score?

Using a secured credit card responsibly may help your credit slightly in the short term, especially when you combine it with other credit improvement strategies. Larger gains will come as you continue to work on your credit over the course of a year or two.

Your credit situation and how responsibly you use the secured credit card will determine how much it improves your credit. Increasing your credit takes time and patience—no credit improvement strategy offers an overnight fix.

Can you increase a secured credit card limit?

Secured credit cards often have low balances, but you may be able to get a credit limit increase. Contact your credit card issuer and ask if you can increase your deposit in exchange for a larger limit. You can also ask if you are eligible to graduate to an unsecured credit card, which typically comes with a larger credit limit.

Work on your credit with Lexington Law Firm

Remember: a secured credit card is a powerful tool to improve your credit, but only if you use it responsibly—spend wisely, pay your bill on time every time and keep your balance low. Take this time to develop a healthy relationship with credit card usage, be patient and trust the process.

If you’re looking to learn more about how to build your credit, the team at Lexington Law Firm can help. Get a free credit snapshot today to get started.

Note: Articles have only been reviewed by the indicated attorney, not written by them. The information provided on this website does not, and is not intended to, act as legal, financial or credit advice; instead, it is for general informational purposes only. Use of, and access to, this website or any of the links or resources contained within the site do not create an attorney-client or fiduciary relationship between the reader, user, or browser and website owner, authors, reviewers, contributors, contributing firms, or their respective agents or employers.